Blog Archives

“To run my business is to run it on Wrike”

Why we are in investing in Wrike

Today, Wrike announced a $10MM Series A funding round led by Bain Capital Ventures. We are thrilled to be partnering with Andrew Filev and Team Wrike! Here are just a few qof the reasons why we are excited to be on board.

Because Wrike is a great product

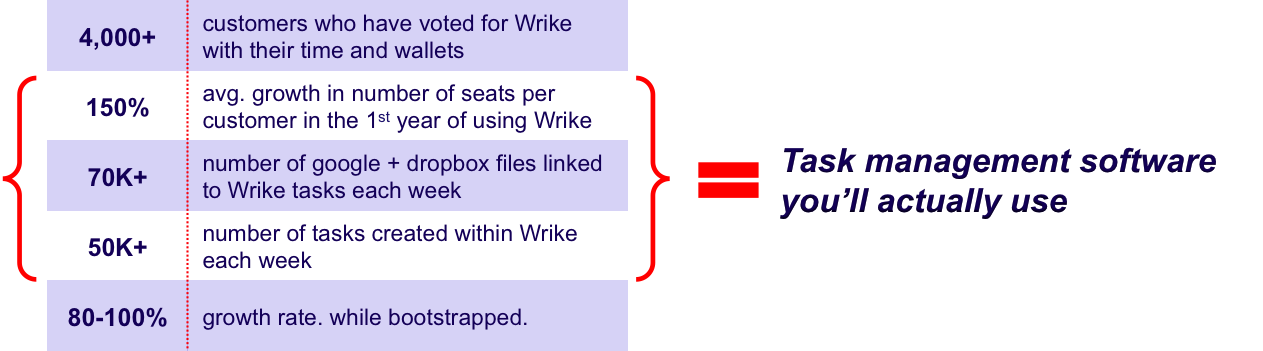

We could tell you that Wrike is a unique product because it adapts to your existing workflows, vs. requiring you to change how you get things done. Or that it sits across task management AND collaboration, vs. just doing one. Or my personal favorite – it works in your email.

But task management software is like ice-cream – everyone has their favorite flavor. So let’s just look at Wrike by the (engagement) numbers:

Being boot-strapped, Andrew and his team had to build a product that users love (and pay for). These usage metrics speak to something special. In the words of one customer:

|

“Wrike is the backbone of our company. It is so integrated within our company that it would be painful – and painful is not a strong enough word – to replace it.” |

Because the “work cloud” needs more connective tissue

Between Google Drive, Dropbox, Box, email, etc., businesses have an incredible amount of data and documents in the cloud. Managing workflows across those platforms is increasingly challenging. Doing so within the app that most knowledge workers live in – email – is even harder.

And the next generation of knowledge workers will be even more cloud centric.

We think Wrike, with its flexible workflows and Drive / Dropbox / Email integrations, can be the connective tissue across those cloud apps.

Because “land-and-expand” is already working

As noted earlier, Wrike customers more than double their number of seats within the 1st year of using the product. That only happens if you have a great product and happy customers.

BCV has a long history of backing companies with “land-and-expand” DNA, including SolarWinds (NYSE: SWI), LinkedIn (NYSE: LNKD), SurveyMonkey, Rapid7, Optimizely and many more. When we see those fingerprints in a company, we know it can be special.

Because it all starts with the people

Andrew and his team have delivered a category-leading product, happy customers and huge growth with no outside capital. And they have built a great company culture with a real sense of mission around empowering their users.

Those are incredible achievements, but we get the feeling that Wrike is just getting started. We are excited to see what this crew does with a full tank of gas!

SaaS Valuations Update

This is an update on the data in my previous post on Software-as-a-Service (SaaS)Valuations. For full context, read the original post here:

Keeping it SaaS-y: Valuations for SaaS Companies

Many of you have reached out to me asking for the source data in this post. Since it’s based on an internal analysis we did at Bain Capital Ventures, I thought I’d share the updated version of the data.

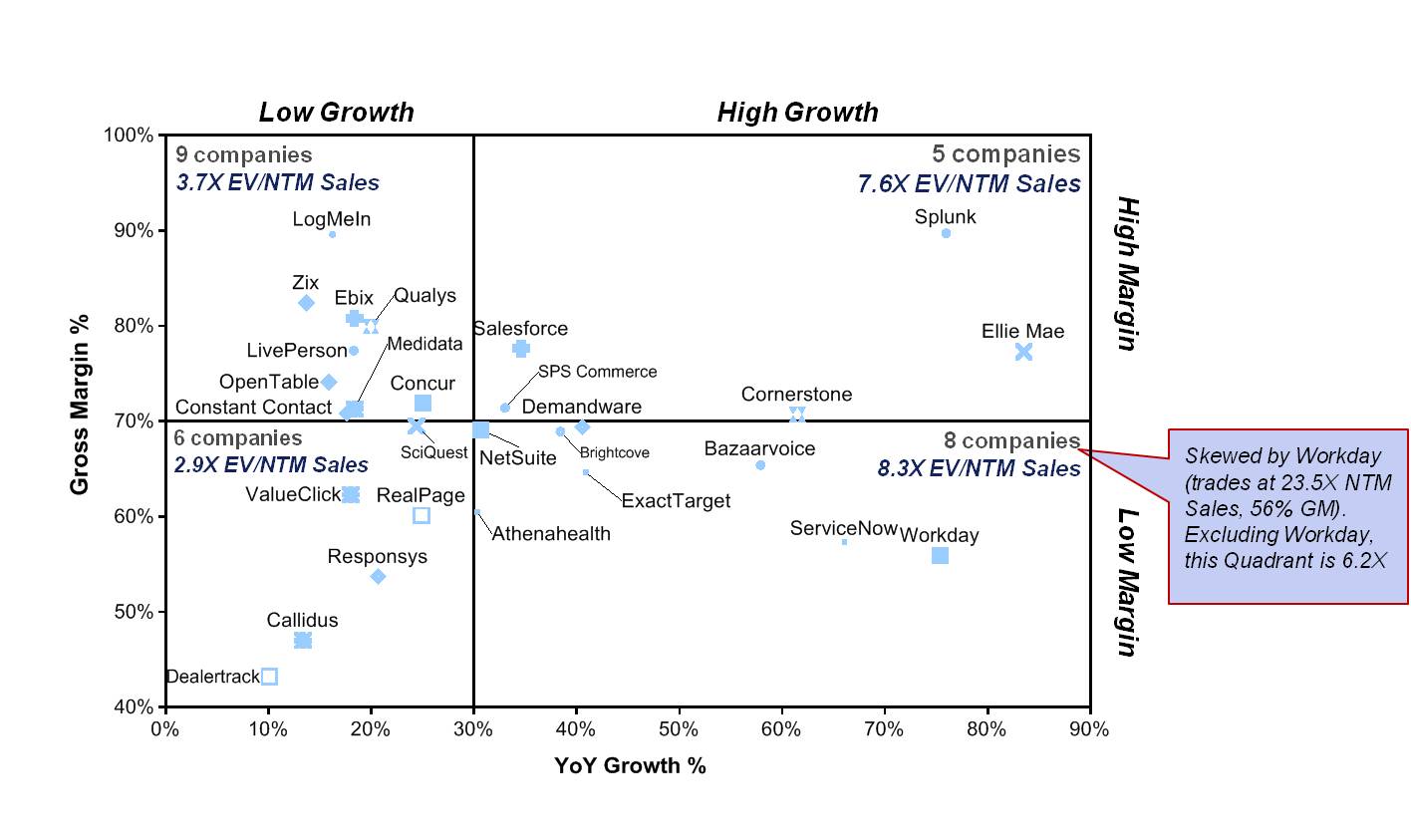

SaaS Valuations Grouped by Growth Rate & Margin (March 2013)

In short, looking across all public SaaS Co’s, high growth (>30% YoY), high gross margin (>70%) companies trade at 7.6X Enterprise Value / Next Twelve Months (EV/NTM) Sales, vs. industry wide average of 5.5X.

In short, looking across all public SaaS Co’s, high growth (>30% YoY), high gross margin (>70%) companies trade at 7.6X Enterprise Value / Next Twelve Months (EV/NTM) Sales, vs. industry wide average of 5.5X.

And growth rate matters more than gross margin. The top-left quadrant (low growth, high gross margin) trades at 3.7X. The bottom right quadrant (high growth, low gross margin) trades at 6.2X, if you strip out Workday.

Keeping it SaaS-y: Valuations for SaaS Companies

But how should you think about valuation? What is “market” for high growth SaaS companies?

Well, here’s one way to think about it:

SaaS Valuations Grouped by Growth Rate & Margin

In short, high growth (30% per year or more) and high margin (65% or more) businesses trade at a big premium. How much of a premium? 7 times your NTM (next 12 months) sales, vs. 4-5 times NTM sales for “regular” SaaS businesses.

Your business (and founder shares) could be worth 40-75% more if you are in that top right category.

Duh right?!? But it raises an important question every founder should care about – how do I get there and what are the signposts?

Some “SaaScid Tests” to live by:

All 3 tests relate to sustainable, high revenue growth:

- If LTV > 3X CAC, every dollar of sales & marketing spend builds strong, sustainable revenue backlog, assuring future growth.

- If months to recover CAC < 12, you are capital efficient (less fundraising and dilution!) and can use your own cashflows to fund your CAC

- Low churn = higher starting point for next years revenue = higher growth rate

If you manage your pricing and your sales & marketing model to these benchmarks, you will enjoy strong profitability. And if you have profitability, you can pursue growth because the customer economics scale.

Oh, and if you’re hitting those benchmarks, we should talk!